Every morning I roll out of bed and ask myself, ‘What should I do today?’

As I write this sentence, I’m looking out over a beautiful beach on an island off the coast of Cambodia. I don’t have a proper job, but my bank balance recently hit six figures.

I won’t lie. These factors may have contributed to my general enthusiasm about life. But there’s another reason I sometimes stare into space and smile at nothing (even if anyone in the vicinity thinks I’m a crazy person).

For the first time in my life, I have absolute freedom to only pursue the things that interest me. The last two decades have been an uninterrupted freight train of schooling and work, so it’s a pretty surreal feeling. There are moments of pure elation, and even the occasional faint trace of guilt. Did I cheat, somehow? Surely it can’t be this easy? I’m waiting for a giant skyhook to descend from the heavens and hoist me up by the seat of my elephant pants, violently jerking me back into reality.

It wasn’t until 2013 that I even twigged this was an option. I’d been working as a business journalist for a couple of years, and one of my responsibilities was researching and writing personal finance features.

I’d chosen the topic of ‘net worth’, which is defined as everything you own, minus everything you owe. Naturally I was curious what my own net worth was, so I did the math.

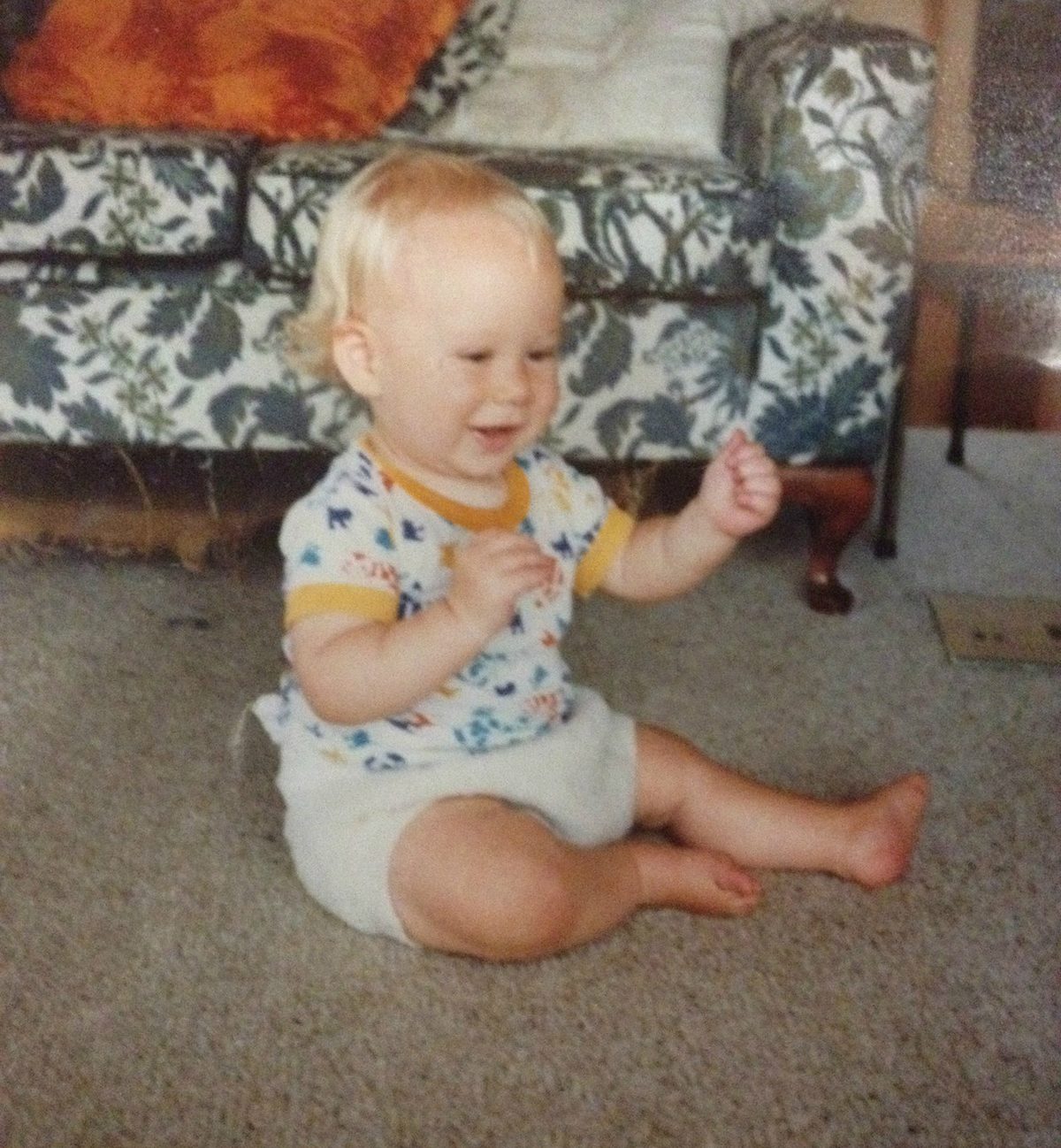

It was a negative number. My savings and other assets were completely wiped out by my debts - and then some. Finding out you’re worse off now than when you first entered the world as a naked, screaming, hairless maggot is kind of depressing.

This little idiot enjoyed eating dirt and pooed himself daily, but he was still more of a baller than me.

It wasn’t much consolation knowing most twenty-somethings were in the same boat, especially those with student loans. Unlike them, I made my living lecturing people on how to be good with money. The first penny dropped. I decided it was time to shift up a gear.

Around this time I’d also started learning about the ‘early retirement’ and ‘financial independence’ movements. It turned out there were cadres of rebels around the world who flat-out rejected consumerism. They laughed mightily at the thought of 40 years of wage slavery, and retired decades earlier than everyone else.

I interviewed one of the rebel movement’s unofficial leaders, Pete Adeney, who saved enough cash to quit work at age 30 so he and his wife could spend more time with their boy.

Another penny dropped. The money habits of Pete and his peers were some next level shit. Conventional personal finance “wisdom”, like the stuff I’d been dishing out, was that you should aim to save 10 per cent of your after-tax income. These guys saved half their pay, or more - and they did it in style.

How to Win the Jackpot

The more I read, the more pennies dropped. Soon they were gushing out like I’d won the jackpot, albeit on the cheapest slot machine in Vegas.

This is the bit where I’m meant to plug my guide to red-hot growth stocks, or sign you up to some scammy forex trading course.

Sorry to disappoint, but there is no magical way of getting rich. While we’re crushing dreams, Santa’s not real, and Margot Robbie doesn’t know you exist.

The true ‘secret’ is simple:

Live on less than you earn. Save and invest the difference, and let compound interest do its thing.

I understand if you’re underwhelmed. Most people already know this, at least on some level. It wasn’t until I saw what happens when it’s put into practice that it really blew my socks off.

Geeking out with Spreadsheets

What gets measured, gets done.

— ANON

Slowly but surely, I reassessed every area of spending. I cut the bloat and wastage. I thought about what was really important to me, and what wasn’t.

Things really started humming along after I customised a spreadsheet to track my net worth. Every month I got a little buzz out of seeing the number climb higher and higher. I could also tell if progress was slowing, and give myself a metaphorical kick in the butt as required.

(Be sure to check out my post on Net Worth Tracking to learn more, and grab yourself a free copy of my spreadsheet.)

Journalism is not known for its lucrative salaries, and I wasn’t exactly earning megabucks. Nevertheless, a shitload of savings poured into my bank account. I needed somewhere to put it, so I started dabbling with investing. After a few initial bumps and scrapes, I figured things out and ended up doing pretty well.

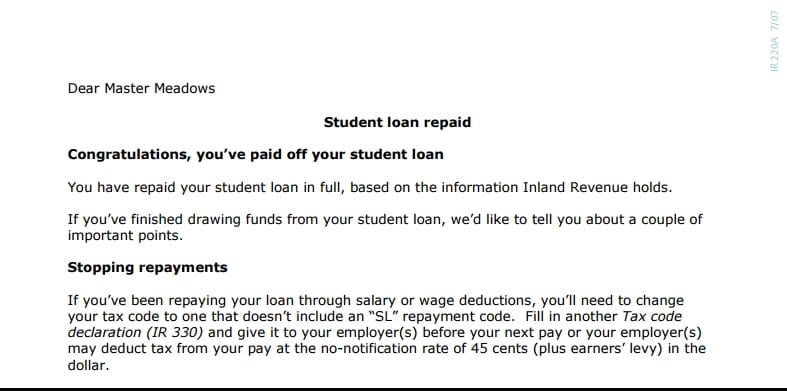

My net worth kept growing, into the tens of thousands. Along the way, this happened:

That’s right, Master Meadows. This letter is even cooler if you read it in Michael Caine’s voice.

In early 2015 I started fantasising about taking an extended break from the 9 to 5, or abandoning it altogether.

I loved my job, especially back when the news industry wasn’t as far down the death spiral. But my feet were itching like crazy. I’d been in the same gig for more than four years. I was losing my mojo. All sorts of personal projects were swirling around my head, but there was no time to make them happen.

So I made a promise to myself: Once my net worth hit NZ$100,000, I’d quit my job, sell everything I owned, and move overseas.

One year later, I was into the ninety thousands. I bought a one-way ticket to Bangkok and handed in my notice at work. I was walking on air by this point, and probably could have saved myself a fare by floating across the Pacific.

When the time came to board my flight, the $100,000 target was still frustratingly just out of reach. A dumb investing mistake had finally caught up with me, setting me back a couple of months. I was mildly disappointed, but too excited about starting my adventure to dwell on it.

On August 1 2016, I was sitting in a KFC in Phnom Penh, mildly hungover. As the good Colonel’s deep-fried gift to the world worked its restorative magic on my gut, I took advantage of the free WiFi to do my monthly net worth update.

The spreadsheet spat out the number $101,227, and I spat out a mouthful of Zinger burger. Halle-fuckin’-lujah! In three-and-a-half years, I’d gone from being penniless to having a net worth of six figures. I stuffed the rest of the burger in my mouth, and relished the taste of grease, mayonnaise and victory.

(Note: My savings goal was in New Zealand pesos, the currency of my home country. To reach six figures as denominated in the mighty greenback took me until the ripe old age of 26.)

What Do You Want?

A man’s worth is no greater than his ambitions.

— MARCUS AURELIUS

$100,000 is a nice round number, but it’s also completely arbitrary. I only chose it because it would comfortably give me enough cash to achieve my actual, underlying goals.

Believe it or not, my aim wasn’t just to lie on a beach drinking cocktails every day and posting obnoxious status updates to Facebook.

‘How’s your Monday going, losers? HAHAHAHA!’ …etc

I can confirm this is incredibly fun, but only for about three days. Down that path lies alcoholism, crushing ennui, and the leather-tanned hide of an elderly rhinoceros.

Here’s what $100,000 really bought me:

- The joys of open-ended travel (OK, including aforementioned cocktails)

- Helping some friends finance their businesses

- Being able to pursue projects that I couldn’t when working full time (like this blog)

- Free time to learn new skills and hobbies, and take existing ones up a notch

Whenever I was tempted to splurge, I reminded myself of what I was working towards.

Maybe your goal is travel, or saving a house deposit, or starting a business, or something else entirely. It doesn’t matter, as long as it means something to you.

The sum of money doesn’t matter either. The exact same principles apply whether you want to know how to save $100k or a cool million. Getting there is only a matter of time and effort - and it only gets easier.

The First $100k is the Hardest…

The first $100k is a bitch, but you gotta do it. I don’t care what you have to do—if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.

— CHARLIE MUNGER

The cool thing about money is that once you have enough of it, it starts making more money all by itself.

In the first year of saving, I earned some modest investment income. The next year, I was earning interest not only on my savings, but on those earlier returns. And so on.

The magic moment. You can see a slight curve as the investment returns start to come into play.

(Check out ‘The Beginner’s Guide to Becoming a Badass Investor’ for an animated guide on getting started with investing.)

Over longer timeframes, compound interest is crazy powerful. Let’s say my goal was early retirement, and I decided to stay in full time work to maximise my savings.

It would only take a little over two years to save the second $100k. The third $100k would come even faster still. Even if I never got a pay rise, I’d be a millionaire in about 13 years.

As it happens, at the time of writing I’m only doing a few hours of (paid) work. Nevertheless, my net worth is still growing. To build that sort of momentum takes a fair bit of initial effort.

…But it’s Not That Hard

Wealth consists not in having great possessions, but in having few wants.

— EPICTETUS

According to the denizens of news website comment sections, anyone living frugally must be a smelly, communist, cheapskate, dumpster-diving hermit. I resent that. I always put on deodorant (to mask the garbage juice smell).

Living simply doesn’t mean being some sort of miserable tightwad. My experience was the exact opposite. Once you have the basics of life covered, money doesn’t really correlate with happiness. The best things in life truly are free, or at the very least, dirt-cheap.

It doesn’t mean becoming a monk, either. I still spent money on travel, eating out, booze, pizza, concerts, and other such awesome things. I just had to figure out how to cut costs wherever possible, and restrain myself a little. Eating at nice restaurants is a whole lot more fun when it’s a treat, not a normal routine.

A little perspective also helps. Anyone reading this is by definition part of the richest and most fortunate cohort in human history. Kings of old couldn’t dream of the technological marvels and healthcare enjoyed by even the poorest among us today. There’s more power in our iPhones than the machines that put man on the moon, but heaven forbid we don’t immediately have the latest model - you know, the one with the dancing poop emoji.

You Do You, I’ll Do Me

Dogs bark at what they cannot understand.

— HERACLITUS

Changing money habits takes some elbow grease at first, but once they’re locked in it’s all gravy. The bigger challenge might be dealing with the expectations of other people.

It’s tough to explain to your mates that you don’t want to do Expensive Thing XYZ - not because you’re a fun-hating scrooge, but because you have different goals and priorities to them.

Those who are most judgemental are usually the same alleged “adults” who are constantly broke and borrowing money from their mums, despite earning good salaries and having no responsibilities.

This is a good opportunity to practice giving zero fucks what other people think of you, which is a useful life skill in general.

It helps once you realise the most outspoken critics are slaves to their own impulses, to marketing, and to societal expectations. Their opinions are worth even less than their bank balances.

Buying Your Freedom, One Slice At a Time

I would rather sit on a pumpkin and have it all to myself than be crowded on a velvet cushion.

— HENRY DAVID THOREAU

Life is all about trade-offs. Frugal people choose to accept fewer possessions and luxuries in exchange for more freedom and time.

Here’s an example. Would you rather buy a flash new car for $25,000, or an ugly but reliable second hand one for $5000?

To me, the answer is screamingly obvious. Saving and investing that extra $20,000 would give you an extra quarter of a million bucks by retirement. Alternatively, you could buy a couple of years of freedom right now to start a business, travel, or learn a new skill.

Someone with different values might prefer having a cool car. As long as they’ve made an informed choice, all power to them.

I worry that people don’t consciously make that choice. I didn’t even know there was one. My careers counsellor forgot to mention I could retire young, if I just rejected the bullshit ‘keeping up with the Jones’ mentality. No-one told me there was an alternative to 40 years of wage slavery, a crippling mortgage, and a big house filled with junk.

I’m not trying to tell anyone how to live, but I do feel compelled to share my own experience. My eyes were opened by people brave enough to strip down to their financial underwear in public, and I’m forever grateful to them. This is my attempt to pay it forward.

73 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply