The key to success lies in knowing how to both strive for a lot and fail well.

— Ray Dalio

-

Marry an accountant, but have occasional flings with rock stars.

-

Lift very heavy weights for a few repetitions, then do lots of low-impact cardio.

-

Work a secure and boring job, while pursuing highly speculative ventures on the side.

-

Ban yourself from highly dangerous activities, but do anything else without restrictions.

-

Completely ignore most personal attacks, while occasionally going nuclear on a random hater.

There’s a common thread running through all these ideas. It’s called the ‘Barbell Strategy’, and I’ve found it to be a useful model for all sorts of big decisions—from my career and work, to health and fitness, and of course, my investment portfolio.

In How Not to Be a Starving Artist, we looked at the career barbells that entrepreneurs and creatives use to manage risk and maximise their chances of hitting the big time. The exact same concept can be applied to investing. To help explain how it works, I’m going to lift the veil on my portfolio so you can see exactly where I’ve chosen to invest my money.

Before we get into it, a warning: This post is aimed at people with at least a few solid years of investing experience under their belts. If you want to follow along anyway, make sure you’ve read my beginner’s guide to investing and passive investing primer, so you’re familiar with the basic concepts and terms.

Obligatory disclaimer: This blog post is meant for educational and entertainment purposes only. Any resemblance to a real financial adviser, living or dead, is purely coincidental. Do not read while operating a motor vehicle or heavy equipment.

Black Swans

“There are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns – the ones we don’t know we don’t know.”

— DONALD RUMSFELD

A quick tidbit of ornithological history: For most of the last two millennia, everyone in the west knew there was no such thing as a swan with black plumage. It was such an outlandish idea that ‘black swan’ became a common expression for something that was impossible. This persisted right up until the Europeans arrived in Australia, and awkwardly discovered they’d been wrong the whole time.

This simple little error of reasoning continues to trip up experts every day, especially in finance. No-one can predict the inherently unpredictable. All the prior data might produce a lovely trendline that can be extrapolated out forever, but a single high-impact event makes a mockery of the whole exercise. To put it another way: A turkey thinks everything is going brilliantly—all the grain it can eat, a comfy roost, loads of friends—right up until Christmas.

The global financial crisis was one of these ‘black swan’ events. While most of the turkeys lost their heads, trader-philosopher Nassim Taleb made a small fortune by positioning himself to benefit from just such a shock. In his books Fooled by Randomness, The Black Swan, and Antifragile, he explains how you can avoid the negative black swans—extremely rare, high-impact events—while positioning yourself to take advantage of the positive ones.

It’s time to build ourselves some barbells.

Introducing the Barbell Strategy

Picture your investment portfolio as a barbell: two big lumps, separated by a narrow bar. On one side, there’s a basket of extremely safe investments. On the other side, there’s a basket of extremely risky speculative plays. The weight is distributed between two extremes, with almost nothing in the middle.

Instead of having a mildly conservative or aggressive investment strategy, you’re both hyper-conservative and hyper-aggressive at the same time. This approach limits your downside risk—the total amount you can lose—while giving you exposure to potentially unlimited upside.

The two sides of the barbell don’t have to be equally weighted. Taleb suggests putting 85 to 90 per cent of your money in ultra-safe investments, like cash. The remaining 10 to 15 per cent should be placed in a whole lot of small, speculative bets—basically, the highest-risk, highest-reward investments possible.

Here’s what it looks like:

Let’s say a black swan event comes along and wipes out the market. The very worst-case scenario sees you take a haircut of 10 to 15 per cent of your wealth, while everyone else loses their shirts. On the other side of the barbell, if one of your bets happens to pay off, you stand to make enormous gains, while everyone else misses out completely.

Being in the middle gives the illusion of safety, but it’s actually the worst of both worlds: you’re still vulnerable to being wiped out by a black swan, while also having no opportunity to tap into the stratospheric gains that swirl out of the same chaos.

The Weediest Noob at the Gym

goodnight sweet vertebrae

If you saunter into the gym and try to pick up Taleb’s 85/15 barbell right out of the gates, you’ll slip a disc in your spine, and end up in chronic pain for the rest of your life. With most of your money in cash or similar, you’d be lucky to keep up with inflation. Foregoing the enormous power of compound interest means you might have to keep working until you die, and definitely sacrifice the dream of an early retirement.

This is a problem of scale. For someone ‘big’ enough, the bets on the 10 to 15 per cent side make up for the stagnant 85 to 90 per cent. Let’s say Taleb’s net worth is $5 million. That means he’s got a whopping ~$750,000 to spread around a diversified basket of highly speculative bets. It’s highly likely that at least one will pay off.

For a small investor, that high-risk basket might only hold $10,000 or $20,000, which is nowhere near enough to play this game. Minimum buy-ins mean you’d only be able to place one or two bets; perhaps a handful at most. The chances of holding the winning lottery ticket are tiny, which means you’ll end up with nothing, while the rest of your money moulders away in the bank.

I’m not saying Taleb’s barbell sucks. The point is that when you walk into a gym, you don’t use the exact same barbell as everyone else. Instead, you choose one that suits your ability and preferences. It’s not the specific weights that are important, but the general principles:

- decide on an acceptable level of downside risk - which will vary from person to person,

- make room for as much upside potential as your personal circumstances allow, and

- stay the hell away from the middle.

To give you an idea of what I mean, I want to show you the barbell that I’ve designed. It’s much better suited to my own circumstances, and may be of interest to other small investors. For reasons that will be explained shortly, I call it the ‘Bastard Barbell’.

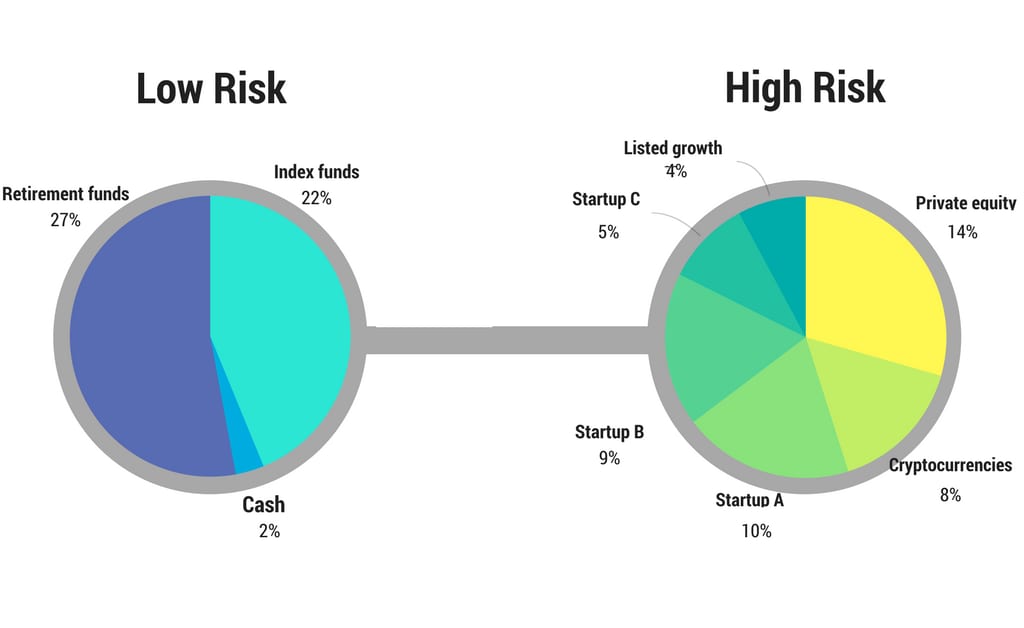

The Barbell Strategy for Bastards

The Bastard Barbell is a mix of low-cost index funds and risky venture capital-style bets. In my case, it’s an even 50-50 split, but you can cut your cloth to suit. Here’s what my investment holdings look like at the time of writing:

Low risk

On the ‘safe’ side, my retirement fund and other money is invested in the most broadly diversified, cheapest index funds I can buy. If any one company or sector fails, it doesn’t make a jot of difference, because I have a tiny slice of more than 10,000 different businesses around the world. I don’t try and pick hot stocks, and will never make more (or less) than the average market return. I’ll be holding this portfolio through thick and thin for the next several decades, and investing steadily into it.

High risk

The other half of my money is in early-stage growth companies, almost all of which are privately owned. I also have a little bit in cryptocurrencies, and a stake in a venture capital fund which owns a basket of New Zealand tech companies. All in all, I’ve placed nine different ‘bets’, or 27 if you include the companies held by the VC fund. I’m going for a multibagger here—only one or two of the bets have to pay off to make up for the rest failing.

As time goes on, most of my new contributions will be focused on the index fund side, which means the weighting of this high-risk basket will eventually adjust to closer to 10 or 20 per cent of my overall portfolio.

Medium risk

The Bastard Barbell avoids the disastrous middle ground of picking individual stocks, or investing in active funds that pick stocks. I learned this lesson the hard way, after putting US$10,000 into a single stock, bang smack in the ‘middle’. It was wiped out by a series of unforeseeable events, and I lost the lot.

Aren’t these speculative VC-style investments just as bad, you ask? The difference is that the return justifies the risk. There’s almost no chance a mature, publicly listed company is going to skyrocket in value. By contrast, a successful venture capital exit is in the realm of 10x or 100x the original investment. These sort of deals are often difficult to access, and don’t have the same disclosure obligations. That means there are opportunities to be found, which haven’t already been priced in by the market.

What’s With the Name?

“Money makes even bastards legitimate.”

— BILLY WILDER

My model is a bastardisation of the barbell strategy in its purest form. Unlike cash or other defensive assets, index funds would still get hammered in a market bust—which means I’m still in the black swan danger zone.

Not only do I believe this is justifiable, I actually think it’s better for me to be a bastard:

- I am young, and have the time to ride out any volatility in the markets. I also don’t need access to any of this money for decades.

- A passive index fund is about as ‘safe’ as it gets in the long run—there’s never been a 20 year period where stocks have fallen. This goes against Taleb’s philosophy, which is that black swans by definition haven’t happened before, but technically the same argument could be applied to fiat currencies or Treasury Bills, or whatever else you consider a safe haven.

- There’s a MASSIVE downside risk in keeping most of your money in cash (it’s just less obvious).

I’m perfectly OK with the ‘safe’ half of my barbell experiencing ups and downs. I own a stake in almost every publicly traded company in existence, and they’re not going anywhere. The only way my portfolio could get wiped out would be some event that literally destroyed every single business on Earth, by which point the skin melting off my charred skeleton would probably take my mind off my investment woes.

I also have no truck with the idea of having to keep working forever because I left my savings to moulder away in the bank. It’s counterintuitive, but failing to take on enough risk is the most dangerous thing anyone can do.

Shooting for the Moon

![]()

The reason I had to give the Bastard Barbell a cute name is that I’ve never come across a strategy like this before. Perhaps this is because it wouldn’t have been possible until very recently.

Traditionally, ‘moonshot’ investments have been out of reach of small-time investors. Venture capitalists made deals with early-stage companies behind closed doors, while everyone else was stuck in the dreaded middle, either playing the stockmarket, or paying a fund manager to do so on their behalf.

Today, it’s still partly about who you know (I’m friends with the founder of one company I’m invested in, and closely involved with its development). But crowdfunding has democratised the VC process by allowing anyone—big or small, connected or not—to get a bite at the cherry. It feels good being an angel investor supporting new companies right from the outset, and helping them make their exciting ideas into reality. The blockchain is another example of democracy in action—anyone at all can take a punt on cryptocurrencies and related businesses.

Obviously, there are major perils: Actual VCs and institutional investors still tend to get access to the best deals, and a lot of expertise is needed to sort the wheat from the chaff (rule of thumb: stick to industries you know intimately, or to founders you trust). As for crypto, don’t get me started.

One option is to outsource the selection process by buying into a venture capital fund. For example, I’m a shareholder in the Punakaiki Fund, which owns stakes in 19 early-stage New Zealand technology firms.

Another way of looking at this is to invest in yourself. You might put 10 to 20 per cent of your savings towards upskilling, or starting a risky side-business. If it does happen to pay off, the returns will be huge.

Caveat

By no means am I suggesting you throw money at your friend’s ‘Uber, but for avocados’ brainwave. I still think buying and holding passive index funds is the way to go for most people, but everyone’s different: with ~60 years ahead of me, I’m a risk-seeker, plus I’m fascinated by the world of startups and entrepreneurship, and enjoy having some skin in the game.

This means my personal barbell is aggressive. I’m in a position where I could afford to lose 50 per cent of my portfolio overnight, and it wouldn’t change my life one little bit. Someone in different circumstances might start out with an 80/20 or 90/10 split (this is roughly where my portfolio will end up, as I reduce my downside risk over time).

Even if you don’t use the Barbell Strategy for investing, it’s a mental model that’s well worth filing away for other aspects of life. By controlling the risk of bad outcomes and increasing optionality for good outcomes, you don’t need to be able to make any specific predictions about what the future holds.

If you’re an aspiring creative or entrepreneur, you might be interested in how it applies to your career. I’ll write a post at some point on its applications in fitness—the ‘barbell barbell’, if you will—and have started a running list of other situations where it’s better to avoid the middle. Let me know if you notice any of your own!

Hyper-aggressively and hyper-conservatively yours,

— Rich

Further Reading

Most investing books are not only a waste of time, but potentially dangerous. Instead of trying to get rich trading Fibonacci retracements or whatever happens to be flavor of the month, I reckon it’s better to wrap your head around the general principles of risk management, behavioral economics, and statistics, and then fill in the details yourself.

Note: The public library will loan you these books for free. If you’d rather buy them, use the links below to send a few pennies to support this site, at no extra cost to you (read more here).

Incerto - Nassim Taleb

Each of the books in Taleb’s Incerto collection stand alone, but I think it’s useful to read them in order. Be warned that Taleb is a bombastic blowhard, takes an unseemly delight in slaughtering sacred cows, and does not suffer fools gladly. Fooled by Randomness is *almost* civil and relatively well-structured, but by the time you get to Antifragile, it’s clearly become impossible for his long-suffering editors to rein him in.

With that caveat out of the way: I enjoy reading Taleb immensely, and these are without doubt four of the most important books I’ve ever read. Fooled by Randomness outlines all the ways in which life and investing are far more random than we realise, and how our attempts to impose meaning upon uncertainty constantly lead us astray.

The Black Swan explores the impact of rare and unexpected events, and how to benefit from the good ones while avoiding ruin from the bad ones.

Antifragile builds on the previous books, and adds the concept of ‘antifragility’— systems that actually improves when exposed to stressors, shocks and failures.

Skin in the Game is a bit more philosophical, with a focus on sharing risks, ethics, and social justice.

All four books overlap in subject and tone, woven together with amusing anecdotes, wild digressions, barbs and vitriol, and obscure classical references. The main ideas have all sorts of applications in science, health, wealth and education, and practical uses for your own life. I can’t recommend this series highly enough.

****The old PDF file of Ray Dalio’s inner musings has acquired a legendary status in entrepreneurial circles over the years, and for good reason. Dalio is the founder of the world’s most successful hedge fund, and this document gives a pretty good insight as to why he’s such a skilled investor. It’s a collection of his distilled principles for life and business - the practical nuts and bolts of how he operates. While the version I read is repetitive and quite clunky in parts, there’s good news: Dalio released an expanded and updated book version in 2017, with the help of an actual writer and editor. I’m looking forward to reading it (if you want the free PDF ‘draft’, it’s here).

11 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply