August 13, 2007: Goldman Sachs chief financial officer David Viniar is sweating bullets. The great credit crunch is in full swing, and Goldman’s flagship hedge fund has lost ~30 per cent of its value in a single week. In trying to justify the huge losses, Viniar tells the Financial Times “we were seeing things that were 25-standard deviation moves, several days in a row.”1

If you paid attention in math class, your eyebrows just shot up so fast that they permanently disappeared into your hairline.

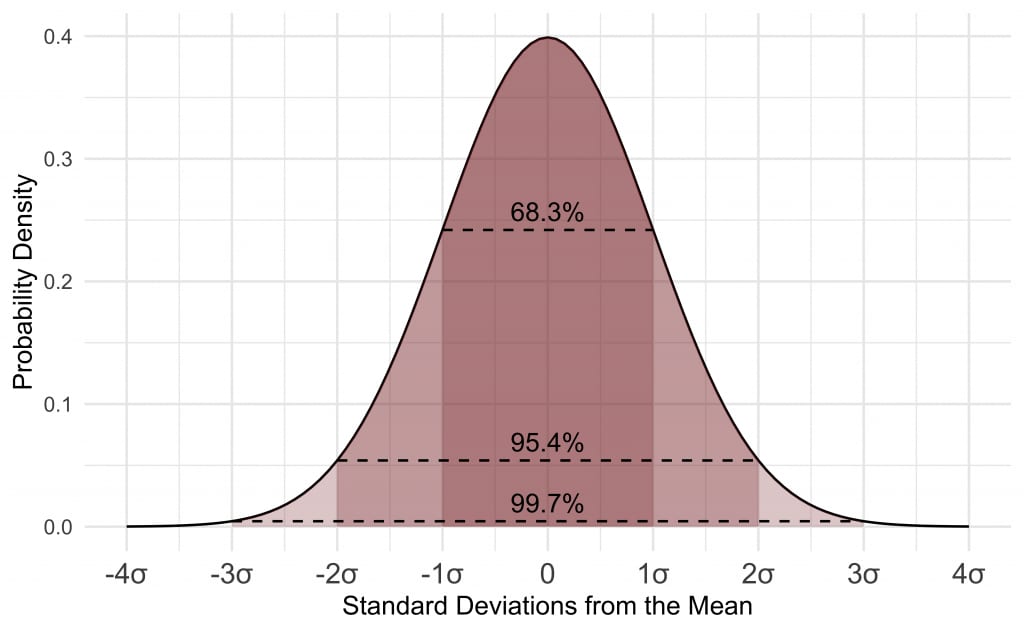

A quick statistics 101 refresher: the bell curve describes how a bunch of attributes—height, IQ, blood pressure, schlong size, the velocity of atoms in a gas—are ‘normally’ distributed.

Like this:

We can see that 68 per cent of events fall within one standard deviation of the average, which mathematicians describe with the Greek letter σ (sigma). Ninety-five per cent fall within two standard deviations, and more than 99 per cent are within three standard deviations.

Anything beyond a 3σ event becomes vanishingly rare, as the tails of the distribution drop off exponentially. The more monstrous the outlier, the more unlikely it is to occur, which means that guy on Tinder is almost certainly embellishing his attributes.

So what are the chances that a 25-sigma event strikes your investment portfolio?

We should expect a 4σ event to happen twice in our lifetime. A 5σ event occurs about every 5000 years, or once since the beginning of recorded history. A 6σ event might have happened roughly twice in the millions of years since homo sapiens branched off from the other apes. A 7σ event comes along every billion years or so, or four times since our planet coalesced out of a cloud of interstellar dust. We pass the Big Bang somewhere around the 8σ mark. At 20σ, the number of years we’d have to wait is ~10x higher than the number of particles in the universe.

By the time we get all the way to 25σ, there are no comparisons that our brains can make sense of without melting into a puddle of goo.

So. Imagine the incredible bad luck of Viniar and friends! Not only struck down by a 25-sigma event, but by several in a row. And of course, Goldman Sachs wasn’t the only company affected. Could it be that the universe served up an entire buffet of events which ought never to have happened in a million billion trillion lifetimes?

Or is it more likely that the Wall Street financiers’ fancy models were… wrong?

The late, great mathematician Benoit Mandelbrot noticed the seemingly impossible happens all the time in financial markets. Crashes, recessions and day-to-day turbulence are jam-packed with ‘freak accidents’, ‘outliers’, and ‘billion-year’ events.

One of Mandelbrot’s PhD students, a certain Eugene Fama2, wrote his thesis on this phenomenon, and found that price movements of more than five deviations from the average happened two thousand times more often than the standard models would predict. A five-sigma event ought to be about as worrisome as a civilization-threatening meteor strike, which might come along once in our recorded history. In practice, these events happen every three or four years.

In other words: the chaotic world of finance cannot be tamed by the cute bell curve you learned about in eighth grade.

The models are finally starting to catch up with reality, although not before they ruined a lot of people’s lives. The only small consolation is that many of the academics who lulled investors into a false sense of security also got blown up, often in spectacular fashion.3

And so, the fact that many people tend to be ‘irrationally’ wary of the markets starts to take on a new significance: the suspicious folk-wisdom has often been correct, while the ‘experts’ have consistently been way too overconfident.

Hence the following warning from Warren Buffett:

Investors should be skeptical of history-based models. Constructed by a nerdy-sounding priesthood using esoteric terms such as beta, gamma, sigma and the like, these models tend to look impressive. Too often, though, investors forget to examine the assumptions behind the symbols. Our advice: Beware of geeks bearing formulas.

All we have is models of the world; all models are wrong; some are useful. The question is: how wrong are the financial models we’re using today?

Dangerously, cosmologically wrong? Or just a teensy bit wrong?

Catching FIRE

up, up, and away

The most popular model we have today: instead of trying to pick hot stocks or sectors, invest in an index fund that tracks the entire market. Instead of trading in and out, buy and hold forever. This is what I’ve recommended for several years. It’s one of the main doctrines of the FIRE (financial independence/retire early) movement, which expands it into the following formula:

- Be frugal as heck

- Pour all your savings into passive index funds with low fees

- Don’t trade in and out, or try to time the market

- Accumulate 25x your annual expenses in investments

- Retire early, and safely withdraw 4 per cent of your portfolio each year without running out of money

Warren Buffett urges us to be skeptical of nerdy-sounding priesthoods, and examine the assumptions behind their models. So, what are the assumptions underpinning FIRE? We already looked at two of them in the previous post:

- The FIRE model works IF you don’t have any uncle points which might force you to sell at an inopportune moment

- The FIRE model works IF you have the intestinal fortitude to stay calm during a major market downturn

Now we’re going to examine another two assumptions:

- The FIRE model works IF market timing doesn’t matter for long-term investors

- The FIRE model works IF historic returns are indicative of future returns

To get right to the point: I think both of these assumptions are shaky, and index funds as a guaranteed way to get rich has been a little overhyped.

Sure, the past returns have been good, on average. Sure, they’re unlikely to go to zero, unless every productive business on Earth simultaneously melts into slag, at which point you’ve got bigger things to worry about. Sure, there’s never been a 20-year period in which the stock market has lost money.

But the standard advice—that timing doesn’t matter—is wrong. Or to put it another way, it’s right on average, but wrong specifically. The problem is that there is no such thing as an ‘average investor’. There’s just you and me, and your auntie, and her neighbour, and a bunch of other individual human beings who care very much about what happens to their precious retirement fund. If your portfolio gets wiped out, it’s not super reassuring to know ‘the average investor’ is doing fine.

Averages are Deceptive

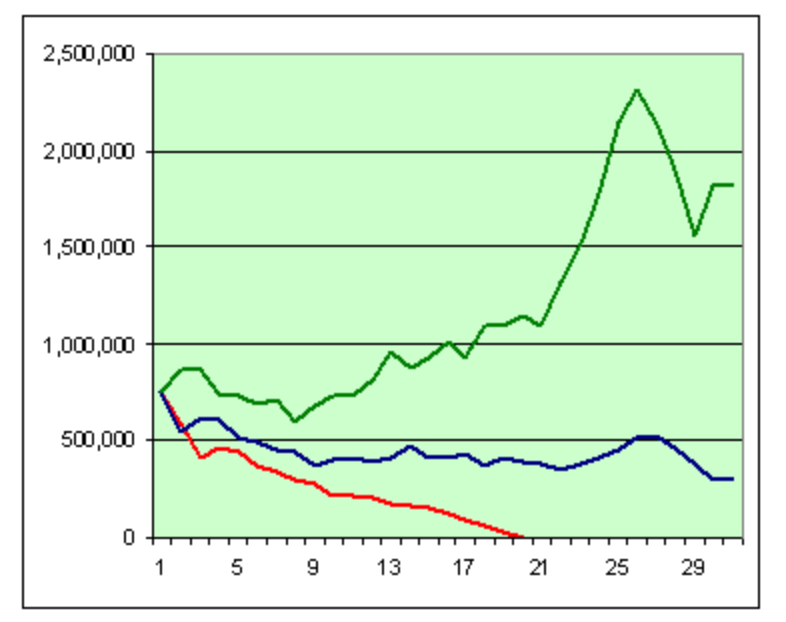

There’s a nifty website called FIREcalc which really hammers this point home. Let’s say you retired in the early 1970s, with a portfolio of $750,000, and planned to withdraw $35,000 of spending money each year. On average, you’ll do very handsomely indeed.

But that average is worse than useless.

Let’s see what happens when three friends with identical portfolios retire in quick succession. Alice retires in 1973 (red), Bob retires in 1974 (blue), and Carol retires in 1975 (green). Here’s how it plays out:

Bob does pretty well, and Carol does spectacularly well. But Alice’s portfolio blows up. It’s incredible how different the outcomes are, based on even the smallest variation in timing.

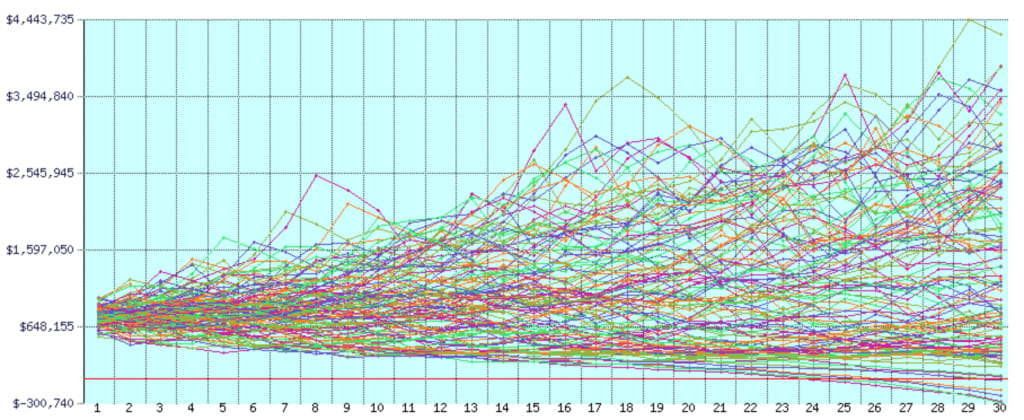

Let’s make the example a little more conservative. If you use the safe withdrawal rate of 4 per cent, that means you can spend $30,000 a year. Let’s take our tweaked example, and apply it across every period of history since 1871. Here’s what it looks like:

Each line represents a different outcome. The highest portfolio balance at the end of the period is $4.25 million, and the average is $1.4m. But once again, the average is misleading. Some of the paths fall below zero (the red line), and the worst outcome is a balance of -$300,739. In 5 per cent of the cycles tested, the ‘safe’ withdrawal rate was anything but.

So: the assumption that market timing doesn’t matter is wrong. It matters a whole lot. There’s a huge variance in outcomes, purely based on luck.

One obvious takeaway is that it’s important to diversify yourself across investing time windows. Unless you invest a big lump sum all at once, this happens naturally: you keep saving and investing a little more each year. If you do that for 20 years, you end up with 20 different investing windows, and 20 different lines on the graph. That way, you become something much closer to the ‘average investor’.

So the buy-and-hold wisdom really shines during the accumulation phase. As long as you don’t hit any uncle points, you’re not eating into your capital during a downturn. And so long as you keep your nerve, you get to keep buying more at bargain prices!

But you can’t diversify your retirement window. It’s a one-off event. From that point on, you only get one line on the graph. Instead of accumulating through good times and bad, you’re burning capital through good times and bad. With a ‘safe’ withdrawal rate of 4 per cent, there’s something like a one-in-20 chance of going bust. And that’s assuming the past has something to tell us about the future.

Does it?

Turkeys Before Thanksgiving

“growth has been strong and steady, and our projections for the upcoming ‘thanksgiving’ quarter are looking rosy…”

Warren Buffett is skeptical of “history-based models”. This is what Nassim Taleb has been banging his drum about for years. There’s a certain type of uncertainty which cannot be measured or tamed. Here’s how John Maynard Keynes put it, way back in 1937:

The game of roulette is not subject, in this sense, to uncertainty… The sense in which I am using the term is that in which the prospect of a European war is uncertain, or the price of copper and the rate of interest twenty years hence, or the obsolescence of a new invention…About these matters, there is no scientific basis on which to form any calculable probability whatsoever. We simply do not know!

No-one can predict the inherently unpredictable. All the prior data might produce a lovely trendline that can be extrapolated out forever, but a single high-impact event makes a mockery of the whole exercise. From the Barbell Strategy for Investing:

To use another of Taleb’s bird-related metaphors, a turkey thinks everything is going brilliantly right up until Thanksgiving. It has all the grain it could wish for, lots of friends, and a warm barn to roost in. Its model of the world is disastrously flawed, but it doesn’t find out until the axe comes down.

We might have an investing winter that lasts 30 years, or a crash that makes everything before it look like a minor fender-bender. Or the current bull run could keep merrily rampaging along for a thousand days and a thousand nights. As Keynes put it: we simply do not know*!* In which case, all the meticulously planned models and safe withdrawal rates are garbage in, garbage out.

The history of finance is a history of brains splattered on the pavement. Over-reliance on flawed models has hurt people over and over and over again. Beware of geeks bearing formulas!

Three Closing Thoughts

Not all geeks are equally dangerous. The early retirement folks don’t deserve to be lumped in with the bankers and financiers who take other people’s money, privatise the gains, and get bailed out when they lose. If the FIRE priesthood are wrong, they will be the first to be hurt. And most of them are already well aware of the nuances described in this post.

Just to make this really clear: I’m a big fan of the movement! Mr Money Mustache ought to be given the Presidential Medal of Freedom. The FIRE model has worked out brilliantly for tens of thousands of people, and I hope it will work out for many more.

The part that makes me uncomfortable is talking about buying and holding index funds as if it were a sure thing, and mentioning safe withdrawal rates without wrapping inverted commas around the word ‘safe’.

If FIRE enthusiasts are a little careless about this—as I have been in the past—it’s kind of understandable. Including endless caveats is boring, especially when you’re trying to ignite people’s enthusiasm. What investing newb would make it through a post like this without their eyes glazing over?

The good news is that none of this actually changes much, in practice. As far as I can tell, the best strategy is still to make long-term investments in cheap index funds and don’t try to time the market. But it does reinforce a few important and under-appreciated points:

First: Take steps to minimise the chances of uncle points. That means insurance policies for income, health, and catastrophic events, so you don’t have to lock in a loss at an inopportune time in the market cycle. It also means forcing yourself to contemplate the end of a marriage, the unexpected patter of little feet, a serious disease or accident, and various other unthinkable scenarios that could cause a sudden increase in expenses.

Second: The safest possible strategy is to maintain diverse income streams that aren’t reliant on investment returns. The ideal is to find work you actively enjoy, and create a life you don’t need to retire from, if at all possible. As my friend Sonnie puts it, he wants to die with his boots on.4

Third: Frugality is the master strategy, always and forever. To use a somewhat unflattering metaphor, frugal folks are hardy little cockroaches: low-slung and nimble and difficult to stamp out. We collect skills. We stash cash. We are perfectly content with a relatively lean existence. We know that nothing is ever promised to us. Should a black swan spread its wings and blot out the sun, those who are trying to FIRE may have to delay their plans, or return to work—but they will be among the best-positioned to not only survive, but thrive*.*

Further Reading

Safe Withdrawal Rate for Early Retirees — MadFientist

This article makes the case that a 4 per cent safe withdrawal rate is pretty much fine, and that even if it’s not, you should know within 10 years of retirement—at which point you can always pick up some part-time work, reduce your spending, or otherwise adjust your plans accordingly, what with being a flexible frugal person and all. I don’t think Brandon’s post conflicts with anything I’ve written above—it’s just a different way of framing the problem, and might cheer you up after reading my somewhat more sober take.

The (Mis)Behavior of Markets — Benoit Mandelbrot

If you were yawning through the statistical parts of this post, probably don’t read this book. With that being said, I found it a handy walkthrough of the evolution of modern finance theory, which finally made all the stuff about black swans and tail risk events really ‘click’. If you like Nassim Taleb’s ideas, you will see the influence here (Mandelbrot was Taleb’s mentor). Also: trippy fractal randomness.

Against the Gods: The Remarkable Story of Risk — Peter Bernstein

This classic delves into the history of probability, insurance, gambling, game theory, Bayesian reasoning, and options trading. It’s pretty dense, but offers up all sorts of interesting gems: did you know there was huge pushback against the ‘infidel’ Hindu-Arabic counting system we use today, to the point where bankers in Florence had to disguise themselves as Muslims in order to learn the new system? Or that Francis Galton’s creepy obsession with eugenics led him to make a bunch of discoveries in statistics?

FIREcalc

I spent the better part of an afternoon playing around with this thing. Click on the tabs at the top to edit your portfolio size, whether or not you’re still working, and tweak various other variables. Then go look at all the pretty lines!

Notes:

Footnotes

-

Goldman pays the price of being big, August 13, 2007. ↩

-

Fama won the Nobel laureate for the efficient-markets hypothesis underpinning the passive investing revolution, as described in How a Billionaire Taught Me to Invest Using the Force. ↩

-

The most notorious example is Long-Term Capital Management, a hedge fund directed by another two Nobel-prize winning economists, Myron Scholes and Robert Merton. It was bailed out in 1998, having lost $4.6 billion and almost caused the collapse of the entire financial system. Whoops! ↩

-

This is why I’m personally no longer interested in FIRE. Having fuck-you money is often enough to redesign your life in the manner of your choosing, rather than spending decades trying to save up enough to buy your freedom outright (although that doesn’t mean it’s not a great option for many people). ↩

14 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply