I have held off on sharing my true feelings about Bitcoin until now, as it soars past its all-time high, so that it will be maximally humiliating when the bubble bursts and all the funny Internet money becomes worthless again.

See, I have something to get off my chest: I don’t think Bitcoin is stupid.

No, not even at these apparently ridiculous prices. Not even when financial illiterates are making grandiose claims about where it’ll end up.

Lots of people have made the case for or against Bitcoin using careful technical or fundamental arguments. I’m not going to attempt that in this post, or regurgitate the basics of cryptocurrency (I’ll suggest some resources later on).

Instead, I want to make two points I haven’t seen addressed elsewhere:

- Bitcoin as a hedge against FOMO

- Speculation as a useful and productive economic activity

Before we get into it: why am I writing about Bitcoin specifically, and not one of the other bazillion cryptocurrencies conjured out of thin air? Or, as Mr Money Mustache asks in his article Why Bitcoin is Stupid, why not invest in his fingernail clippings instead?

They may have no intrinsic value, but at least they are in limited supply so let’s use them as the new world currency! Why not somebody else’s fingernail clippings? Why not one of the other 1500 cryptocurrencies?

Shut up, just send me $100 via PayPal and I’ll send you a bag of my fingernail clippings.

Bitcoin as Crystallised Trust

It’s true that bitcoins have no intrinsic value, but this is not quite the slamdunk that MMM thinks it is. Our entire civilisation is built on abstractions that only exist in the hallucination of our shared social reality. ‘Money’ and ‘human rights’ and ‘justice’ are not natural forms woven into the fabric of the universe. They exist only because there’s a critical mass of people who believe they exist.

MMM is also right that there’s nothing special about Bitcoin in particular. The protocols it uses are not a secret, and can be copied and adapted by anyone. Bitcoin could be dethroned by any of thousands of rivals.

But the reason we might expect Bitcoin specifically to be a store of value is very simple, and requires no analysis whatsoever of its competitors: momentum.

So long as nothing disastrous happens to the protocol itself—and as far as I understand, that’s essentially impossible (EDIT: see the top comment by Norswap for plausible disaster scenarios) Bitcoin doesn’t have to do anything to outcompete. It’s already accumulated 12 years of crystallised trust and belief, which is an eternity in digital time, and makes it extremely difficult for new challengers to get a foothold.

this bubble sure is taking its sweet time to burst

Bitcoin’s first-mover advantage and network effects are not a ‘nice-to-have’. That’s the entire value proposition. The desirability of Bitcoin comes from the fact that so many people are invested in it, doing the mathematical work to keep it secure, and so on.

So: you don’t have to believe in Bitcoin to understand its value proposition. You just have to believe in belief.

Bitcoin as Digital Gold

What’s Bitcoin good for? I like the comparison to ‘digital gold’. It’s not super convenient for daily transactions, just like it wouldn’t be ideal if you had to carve off a bit of your gold ingot to tip the Uber Eats guy. Instead, it’s a durable asset with built-in scarcity, which acts as a reserve or back-end for many smaller transactions batched together. This is how central banks and nations have used precious metals since forever.

Gold is pretty and has some industrial uses, but its value proposition is almost entirely based on this use case, i.e, thousands of years of social proof. It’s a gigantic pain in the ass to transport, divide, store, and secure—dimensions on which Bitcoin is massively superior—but it’s still worth about $10 trillion. So it’s not crazy to expect that Bitcoin might takes some market share from gold as a longterm store of value.

Except…I don’t like gold, either! As I’ve pointed out before, gold is not really a hedge against inflation, or a good longterm investment, or great as a countercyclical asset class.

I am very much in the Warren Buffett camp of not wanting to invest in non-productive assets that just sit around gathering dust. The only way you can make money from gold is by finding a greater fool who is willing to pay even more for a pretty but fundamentally useless lump of metal.

Sounds an awful lot like speculation to me. But is that really such a bad thing?

Speculation is Not a Dirty Word

Here’s MMM again:

When you make this kind of purchase, which you should never do, you are speculating, which is not a useful activity.

I am always going to tell you that price speculation is a bad way to spend your life. This part of it is ideological to me: You Must Earn Your Money By Creating Value for Everyone.

I am very sympathetic to this argument, and feel pretty much the same way. I’ve been highly critical of forex, penny stocks, and trading in and out of equities, because these are zero-sum games: you can only win at someone else’s expense, and once you factor in transaction costs, the game becomes negative-sum.

But an ideological belief is a dangerous thing. I’ve reluctantly come around to the idea that speculation is not zero-sum, albeit in a clumsy and horrifyingly wasteful kind of a way.

Here’s the relevant passage from a 2017 article I wrote about the crypto boom:

While this is going to cause a lot of hurt for a lot of people, the boom and (impending) bust of the ICO bubble is sort of a good thing. The speculative period during the early adoption period of new technologies helps attract a flood of capital, with at least some of the profits reinvested in the platform. Greed is the perfect vector for raising awareness, with a wave of FOMO rippling through society until even your grandma is sending you texts about the price of Ether.

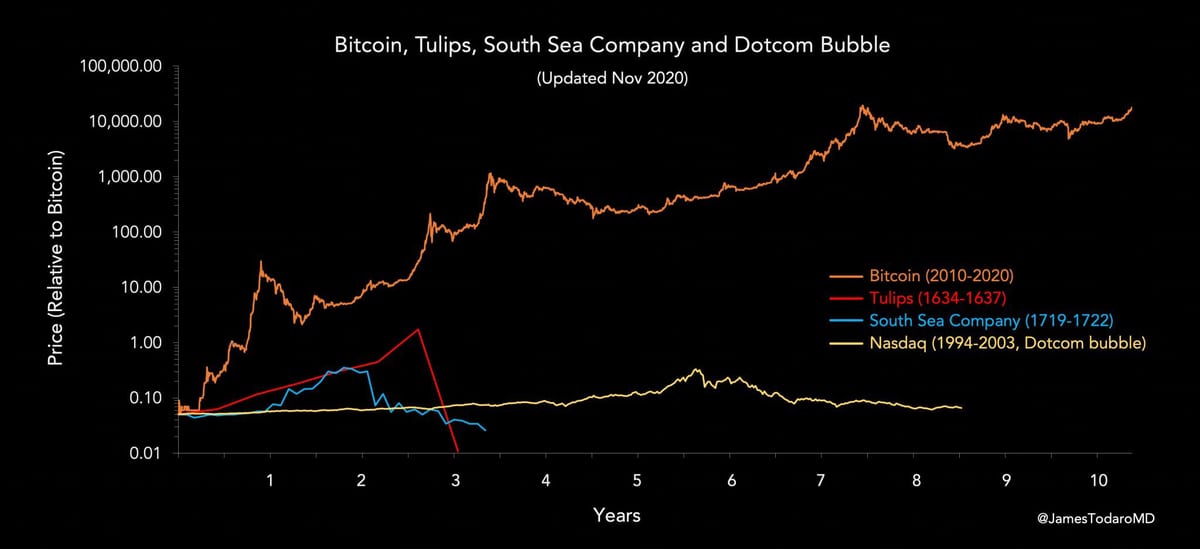

The dot-com boom was one of the biggest bubbles in history, but that didn’t mean the web was not, in fact, a huge deal. […] The hype was real, but there had to be a big painful consolidation before we could unlock the real potential.

The same is true of crypto. The financial system is long overdue for an overhaul, and people are right to be excited about that. It wouldn’t be surprising if some application of blockchain technology became as ubiquitous as the personal computer and the Internet, both of which were originally pooh-poohed by sneering critics who failed to see the writing on the wall.

The Dotcom comparison still looks good to me. Most of the shitcoins have been sent to the crypto graveyard, while the quality ideas—the Amazon.com equivalents—are doing better than ever.1

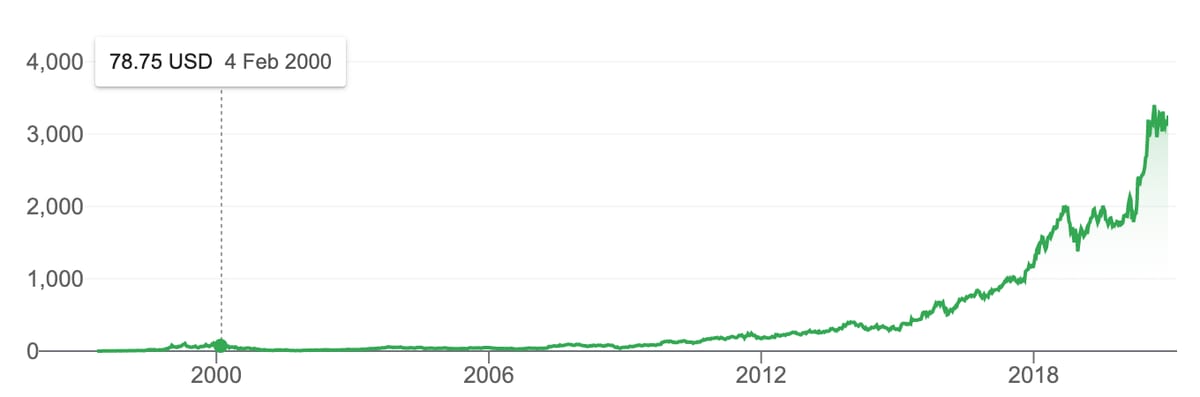

even if you bought Amazon stock at the very top of the dotcom bubble, you’d be sitting on a 4000% return right now

As I suggested in the book, through gritted teeth, one potential black swan hunting ground is speculating on emerging asset classes where you have some unique insight. Of course, it’s too late for that now. Bitcoin early adopters are mega-rich; we don’t have the same kind of upside available to us.

(I started buying crypto in 2017, around the same period as I wrote the Spinoff article quoted above, although you probably wouldn’t guess from reading it.)

But even us Johnny-come-latelies are, in a loose sense, playing our part in ushering in a new age. And if you consider that only something like 1% of the world’s population owns Bitcoin, maybe we’re not all that late.

So let’s do the whole upside/downside thing.

The Asymmetric Opportunity for Bitcoin

Here are what I see as the three main scenarios for upside:

1. Boring bluechip

For me, a modest upside would be anything up to a 10x return, i.e. the price hits ~$200,000. This is what happens if Bitcoin becomes the dominant digital store of value, takes some market share off gold, and becomes a ‘bluechip’ with lower levels of volatility in each subsequent cycle.

2. Hyperinflation

Personally I think this gets way too much attention (Venezuelans or Zimbabweans might feel otherwise). Modest inflation or stagflation is a much bigger consideration, albeit not as spectacular in terms of upside.

3. Global reserve currency

This is the moonshot one for me. The Fed’s printing money like the greenback’s going out of fashion, which… it just might be?

every other country who has to wear the devaluation of their assets may not put up with USD hegemony forever

We know it’s possible for the global reserve currency to change, because it’s happened before: first with the pound sterling, and arguably with gold. There are various candidates for a replacement, but Bitcoin is certainly in the mix. It’s interesting to note that China is already breaking its reliance on USD by building its own digital currency to transact on, and central bankers in dozens of countries are planning similar moves. If a central bank starts actually buying bitcoin, hold onto your butts.

Now for the potential downside scenarios:

- Every universe in which none of the above three events happen, in which case, your bitcoin will be worth approximately zero dollars.

What probabilities should we assign to each of these scenarios? I was tempted to do this, but I’d probably just end up working backwards to justify my beginning intuitions.

Instead, I’ll make a couple of general statements:

- I believe Bitcoin is much more likely to fail than to succeed

- I believe the expected value (EV) of the bet is still positive

Some bullshit numbers for the sake of illustration: if Bitcoin fails in four out of five possible worlds, it has to make at least a 5x return in the final world for the EV to come out positive overall.

I think that’s more-or-less the position we’re in: bitcoin will probably fail, but in the event that it wins, it wins big, and even the current prices will look astonishingly cheap.

So we can still get exposure to potentially asymmetric returns. To be clear, they’re not all that attractive: early adopters were the ones who got the really life-changing upside. But I still think it’s an OK speculative bet to add to a portfolio with an allocation for these kind of positions, e.g. the bastard’s barbell (see the post, improved upon in the book).

What does that mean, practically speaking?

How Much to Invest in Bitcoin

Is Bitcoin stupid? Absolutely, if you do any of the following:

- Having an exposure that is more than single digits of your portfolio

- Trading in and out constantly

- Taking on personal debt to load up

- Other variations of outright gambling, e.g. punts on shitcoins

We have to remember the difference between expected value and expected utility—we can’t bet the farm on a single idea, even if we think it has a very large EV, because in all the worlds where it doesn’t pay off, we’re screwed.2

The general consensus is that someone who is in a comfortable financial position might take a position of about 1-2% of their net worth—an amount of money you can afford to lose without changing your quality of life—and then hold it indefinitely. (This is what I’ve done.)

But when we look at what the sensible advice actually means in practice, there’s something interesting that no-one’s really talking about.

If you do the only responsible thing, which is to limit exposure to a small portion of your portfolio, even a 10x return is not going to have a transformative impact on your fortunes: ($100k net worth * 1% stake * 10x return = $10,000, whoop whoop). We’re going to need another order of magnitude to start getting the kind of asymmetry that doubles our net worth, and that’s way out in the wildly-unlikely branches of the multiverse.

In other words: there’s no way to get stinking rich here, without taking on an inappropriate level of risk through the aforementioned leverage, trading, large exposure and shitcoin gambling. The ship has already sailed; our upside is just not all that attractive.

Which is why I say that the strongest case for bitcoin right now is not actually a transformative financial return—it’s a hedge against FOMO.

Bitcoin for Hedging Regrets

Fear of missing out (FOMO) is what drives ‘dumb’ money to pile into asset bubbles. This is largely what fuelled the last hype cycle; no doubt the same thing will happen again in this one.

My slightly edgy take is that people with FOMO are not necessarily behaving irrationally from a psychological perspective, given the constraint of limiting exposure to a small % of net worth.

What do we know about regrets? You regret the things you don’t do more than the things you do. If you invest in Bitcoin and it goes bust, you probably won’t regret it so long as you’ve framed it as play money that won’t change your life outcomes. If you invest in Bitcoin and get a 10x or a 100x over years/decades, you will feel smug and ‘in the loop’ and get to brag about how early to the party you were, even if you were kinda late and it was only ever a small percentage of your net worth in the first place.

This is similar to the phenomenon in which status-hungry rich people try to get a tiny slice of a unicorn company at series C/D/E long after it requires any kind of brilliant insight, so that they can put ‘early investor in Uber’ in their twitter bio. Is this lame? Yeah, but they still get to brag about it.

So here’s my actual framing on Bitcoin: it’s primarily a hedge against FOMO/having to eat crow, with some minor benefits in terms of diversification, inflation scenarios, corrupt governments, and so on.

I’ve owned crypto for more than three years, and have started buying more seriously in recent months. So why did it take me so long to come out and actually say so?

Respectability and Bitter Nocoiners

If you read my article for the Spinoff you’ll notice I was fairly acerbic—mostly about ICOs, on which history has proven me right, but about the broader phenomenon too, where my public position didn’t entirely match up with my private actions.

Why? Partly it’s a matter of responsibility: as a journalist, you have a duty to be skeptical and make sure your readers don’t get rekt.

But there’s also a social consensus thing going on. The respectable mainstream position is (or was) that this is dodgy online money used by criminals and hucksters. Except…that’s wrong.

Anyone who has been paying the slightest bit of attention knows this is not true. Hedge funds are in. Major banks are in. Billionaires are in. Paypal is in. Serious investors are in. If and when a boring-ass central bank starts holding some of its reserves in crypto, the salty nocoiners who still think it’s all a big scam are going to look pretty silly.

Why are former skeptics not updating on this? Maybe they’re still right and the new evidence doesn’t change anything, or maybe it’s confirmation bias. Personally, I’m relieved I didn’t write crypto off entirely, a la MMM ( “We’ll start with the answer: No, you should not invest in Bitcoin.”) or the drive for internal consistency might have prevented me from being able to reevaluate that position.3

It’s easy enough to overcome the social respectability thing privately, as I’ve been doing for the last few years, but very hard to do publicly. If Bitcoin ultimately fails, then everyone will tell you how dumb you are, MMM will write another triumphant article about his toenails, etc. And remember that this is the most likely outcome! So you have to be OK with that, although so long as you keep your business to yourself, you’re good.

In any case, I’m secure enough in my position not to mind what strangers think of me.

The aim of this article is to add my own tiny bit of social proof to the whole enterprise, and offer a counterpoint to some of the other voices in the personal finance blogging community who have led their readers to miss out on the best performing asset class of the decade, and are currently in the process of doubling down on their position.

Bitcoin is kind of stupid, but it’s also kind of awesome. Ignore the relentless shills and the hardcore haters. The truth lies somewhere in between.

Notes:

Footnotes

-

Bitcoin has baked this hype cycle into its very structure, with its regular halving of supply all but ensuring it would get headlines with each boom and bust. Crucially, volatility contracts with each subsequent cycle, and credibility/trust builds. I don’t know if this was deliberate, but if so, it’s genius. ↩

-

If all this EV stuff is going over your head, see Chapter 22 of Optionality for the full explanation. ↩

-

I love MMM’s stuff but his ‘fingernail clippings’ take was honestly not great, and he’s still doubling down on it—this being the kind of narrow prescribed ideology that makes me somewhat less enthused about the FIRE movement. ↩

24 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

- Computer hardware, firmware and software; e-commerce software enabling users to carry out commercial transactions by electronic means via a global computer network;

- application software for block chains;

- software for purchase, sale, management, payment, downloading, recording and administration of tokens;

- payment cards;

- spare parts, accessories, software and firmware for all the above-mentioned goods.

- Financial affairs; monetary affairs; banking services; credit card and debit card services;

- verification, analysis and evaluation of payment transaction data (financial services);

- financial information concerning foreign exchange transactions;

- financial information concerning currencies;

- issuance and redemption of tokens;

- foreign exchange trading operations;

- foreign exchange trading;

- money transfer services;

- processing of electronic payments;

- management of real estate assets of electronic tokens (e-wallet);

- financial services provided by electronic means;

- cryptocurrency services, namely, a digital currency or digital token, incorporating cryptographic protocols, used to operate and build applications and block chains on a decentralized computer platform and as a method of payment for goods and services.

- Programming services in the field of information technology in connection with software for e-commerce;

- design, development and implementation of software in the field of block-chains;

- provision of advice and services provided by consultants relating to software;

- provision of computer programs for e-commerce.

- Provision of user authentication services in the field of e-commerce transactions;

- provision of user authentication services in the field of e-commerce transactions on communication lines.

Notice it doesn't exclude bitcoins. It does integrate them. Notice also that it acts as the gateway for issuing and redeeming of digital tokens. It will be interesting to see how this evolves, especially with China doing a similar thing. (Russia appears to be sitting on the sideline, and how India will cope is a mystery. 'Trust' in India is the gold bangles on women's arms.)Show 2 replies Hide replies

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply