This might sound gauche while people are dying in horrifying ways, but people are constantly dying in horrifying ways, and besides, I know you’re thinking about it.

Apocalpyse scenarios crank up the dial on all three of the human emotions: fear, hunger, and horniness.

I already ate all my emergency snacks by day two of quarantine and this is a family-friendly blog, so let’s stick with ‘fear’.

It’s hard not to be scared about your financial future, especially if you a) just lost your income source, or b) are currently missing tens of thousands of dollars from your investment account.

I can’t do much about the first one.1 The stretch goal of this post is to get those dollars back in your investment account, and then a whole lot more besides. The modest goal is to prevent anyone from accidentally blowing their own foot off.

‘Managing to avoid shooting yourself in the foot’ is not hugely inspiring as far as aspirations go, but I’m convinced that it’s the secret to winning in life.2

There are a couple of cheap/free options you can to take out to limit the near-bottomless downside risk of COVID-19. I mentioned them in The Inevitable Coronavirus Post but they’re time-sensitive; hopefully you took those steps before the panic-buying and lockdowns began.

Now it’s time to think about the upside. When a black swan flaps its wings, great risks and opportunities swirl out of the same chaos.

What would it take to not just weather this situation, but profit from it?

Taking the question broadly: there’s a bunch of status up for grabs. A few online communities and individuals who were front-running this thing have seen big increases in their audience and platforms, and deservedly so—they profited from the willingness to be weird in the face of intense social pressure to sit patiently while the room fills with smoke. Meanwhile, the incredible incompetence of most authority figures and institutions has revealed that there are no grown-ups in the room. These dynamics are fascinating but not exactly Actionable Content, so let’s leave that for another time.

In the narrow financial sense: I think it’s possible to make some serious money from the coronavirus crash.

The first thing to note is that the bar has been set unusually low. Normally, when stocks tank, other assets go up, meaning there are plenty of winners crowing about their prescient investing decisions.

The incredible thing about this crisis is that no-one is winning. Bonds are falling. Gold is falling. Bitcoin is falling, even as the money printers go brrrr. Even frickin’ Treasuries no longer look like a safe haven.

In short, every liquid asset is getting punished. People are selling everything up to and including the kitchen sink, stripping the copper wiring out of the walls, breaking the house down for scrap, then auctioning off the ground beneath it, etc.

This is mostly just a curiosity for finance wonks and economists to puzzle over (feel free to enlighten me in the comments). For our purposes, it means we don’t have to worry so much about how the Joneses are doing. No-one’s making bank right now; not even those dudes who tried to price-gouge 18,000 bottles of hand sanitizer.

The second thing to note is that some investors are pretty much screwed. There is no sugar-coating this, so we might as well get it out of the way first.

Don’t Make Plans While Being Punched in the Face

Everyone has a plan until they get punched in the face.

— MIKE TYSON

This is a great quote but it’s nowhere near pessimistic enough: hardly anyone has a plan to begin with!

Are contingency plans tough to stick to? Yes. But having a plan in advance is still much better than trying to come up with one while being repeatedly punched in the face. You’re in fight-or-flight mode, your brain is bouncing around your skull like a pinball, your amygdala is stewing in a marinade of fear and adrenaline.

Looking back at this moment many years from now, how sound do you think these decisions will be?

carefully considering the relative merits of long volatility vs traditional asset allocation

Instead of trying to make life-changing decisions in the midst of market mayhem, you should just stick to the plan you prepared at some point during the last 10 years of good times. Which is totally a thing that everyone did. Right?

…Right?

HA HA HA HA HA HA HA HA HA HA HAAAAAAAAAAAAA

*wheezing segues into panic attack*

OK. Excuse me; this is therapy for me. Once again, here’s the relevant quote from If the Market Crashed Today:

When the crash comes, can you brave a 30 per cent decline without flinching? What if it happens in the space of a couple of days? How will you sleep at night? Do you have an ulcer? No? Do you want one?

I think it’s a good idea to visualise these kinds of scenarios in as much detail as you can, and really try to ‘feel’ it. Be honest with yourself about how you might respond in a crisis. Maybe it makes sense to take some money off the table, or have a portfolio that isn’t 100 per cent in stocks, even if it’s technically not the best strategy.

If you didn’t take this advice, well… you really should have taken this advice, but that’s OK. All is not lost!

That is, assuming you don’t need your money out any time soon:

Less than five years: what the heck are you doing in the sharemarket? Less than 10 years: still a bit iffy.

For those who ignored this piece of advice, repeated ad nauseum in every investing 101 article since the dawn of time, there is no ‘good’ strategy for getting out of this with your hide in one piece. Sorry.

Anyone who needs their money out in less than 10 years is now in the unenviable position of trying to time the market.

Timing the Market

that is the question

As at the time of writing, the S&P 500 is down 30 per cent from recent highs. To put it in context, that’s three year’s worth of gains wiped out—a big deal, but not disastrous in the context of a decade-long bull run.

If you sell out, you’re locking in that loss. Maybe this is as bad as it gets, in which case it’s better to ride it out and catch the rebound.

On the other hand, maybe there’s a whole lot more pain to come: markets tanked 56 percent during the last crash, and 86 per cent during the Great Depression.

So, what to do? How long will it take to come out the other side? Is this a quick in-and-out adventure? A V-shaped recession? A long, grinding, decade-long depression?

I don’t know, and anyone who claims to know for sure is lying or deluded.

This is the most important sentence I will write, so read it again: I don’t know how long this will take, and anyone who claims to know for sure is lying or deluded.

Now, a few lucky souls will make their exit with perfect timing, and get back in near the very bottom. Doesn’t that mean they outsmarted the market?

Remember that you’re far more likely to hear from these people, who are under incredible internal pressure to believe they are brilliant gurus, than everyone else who tries to be clever and gets the spanking they deserve. This is called survivorship bias, and it’s just one of many cognitive pitfalls which makes investing a deadly honey trap for smart people.

If you are smart, you might think you can use your big juicy brain to quickly become above-average in many areas of life.3 This is sometimes even true! But oh man… not when it comes to investing. In publicly-traded markets, even the smartest people are like ants, trying to outsmart the closest thing to a superintelligence humankind has ever created.

I’ve previously written a bunch about passive investing, trying to catch a falling knife etc, so I’m not going to labour the point.

Timing the market is risky business. You have to get lucky twice: on the way out, and on the way back in. If you have no choice but to try anyway—maybe you need to preserve your capital for a house deposit, near-term spending, or an unexpected emergency—I sincerely wish you all the best. It’s a crappy situation to be in.

Everyone else can breathe easy. No need for a Hail Mary. When the streets are running red, it’s those who don’t try to time the market who reliably make big bucks.4

How big are we talking? I think perhaps quite a bit bigger than many people would expect. Let’s have a look.

The ‘Big Brass Balls’ Portfolio

I was too shy to get a picture, but I enjoyed rubbing the enormous bronze testicles of the Charging Bull when I visited NYC, as is the local custom, while thinking about getting rich (the other local custom)

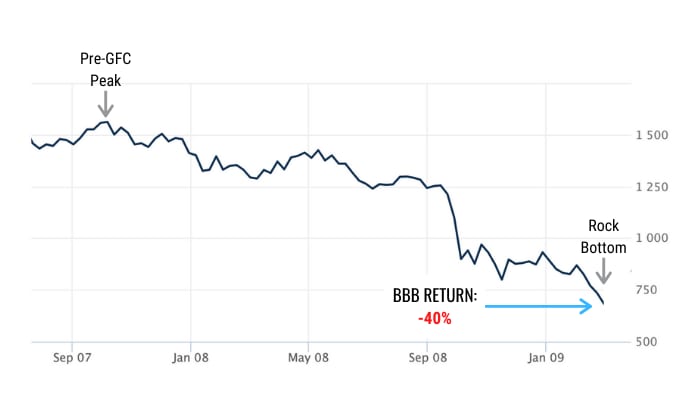

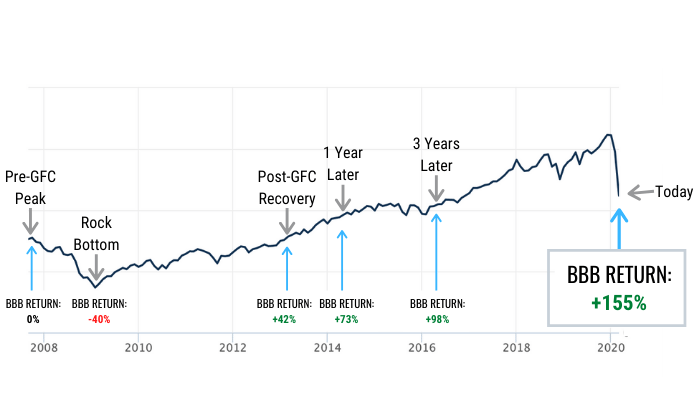

During the global financial crisis, the stock market was cut in half. It took ~65 long months to get from the pre-GFC peak to the eventual recovery. What happened to those brave souls who kept faithfully investing throughout the chaos?

Let’s call the stocks bought during this period the Big Brass Balls portfolio, or BBB for short.

You start accumulating in November of 2007, while the world is on fire and everyone is freaking out. On the first day of each month, you buy more stocks, and reinvest any dividends.

To begin with, your strategy looks terrible. Almost every month, your returns drop further into the red. After a year and a half, things have never looked so bad:

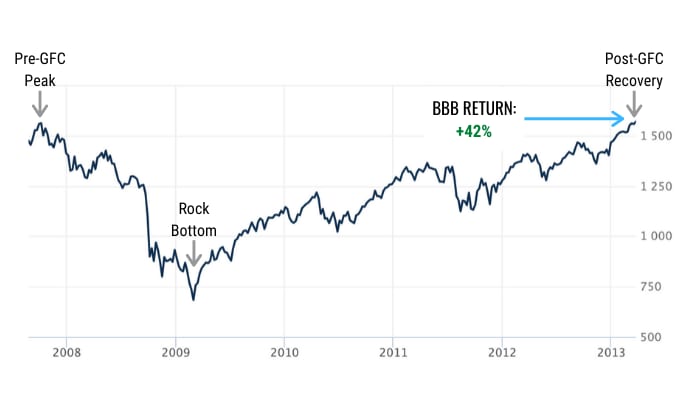

Then the recovery begins. By April 2013, the S&P 500 has finally wound its way back to where it was pre-GFC. Womp womp.

While the headline index has moved 0 per cent in almost six years, that’s a deceptive indicator. It doesn’t include the impact of reinvested dividends, or the fact that you’ve been consistently buying in at discounted prices. And so, while most people have made hardly anything in this period, your BBB portfolio has appreciated by 42 per cent:

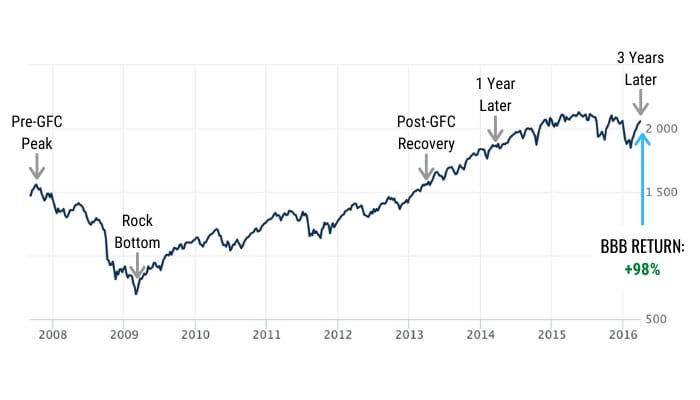

This is already pretty great, but the real payoff is yet to come. One year later, your BBB stocks are up 73 per cent. Now, they’re starting to seem like a bargain.

Three years later, they’ve almost doubled in value. Now they seem like a fantastic bargain:

How about right now?

It feels like the world is teetering on the brink of collapse, but those stocks are still up…155 per cent.

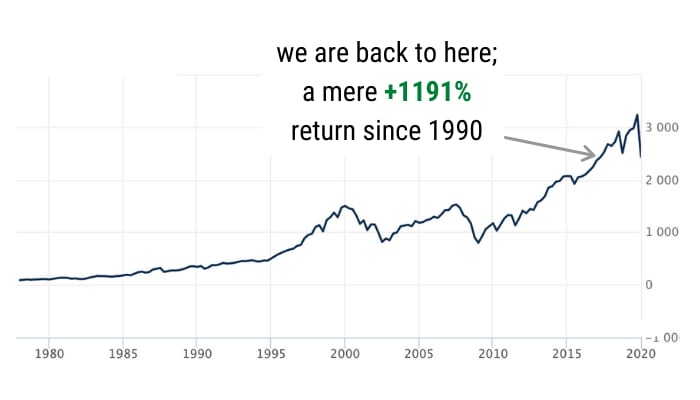

Let’s zoom out once more, just for fun, and put the current crash in its proper context:

The BBB portfolio generated an excellent return through the previous crisis, even though it uses the simplest possible strategy.

There is a very good reason why ‘buy and hold forever’ is the gold standard in investing advice. It requires zero attempts at timing the market, zero clever ‘insights’, zero knowledge, zero luck—and if you do it right, zero self-discipline.

Four Possible Failure Modes

How might the classic buy-and-hold advice fail us? I can think of at least four ways:

1. Losing Your Nerve

This is my first proper crash, so I don’t know how psychologically demanding it is to keep buying the dip. Early signs suggest I’m as yellow-bellied as anyone, but I’m confident I will ultimately take my own advice. For many seasoned investors, who have already been through this three times, this is old hat.

Can we protect against this failure mode?

Yes! Set up an automatic direct debit to your broker, ban yourself from ever looking at your account, and go about your life as normal. Then you can take all the anxiety and fruitless efforts to time the market and use it to fuel more interesting neuroses, like that weird-looking mole on your arm.

2. Crying ‘Uncle!’

Even if you know you have the intestinal fortitude required to see this through, the universe has a way of messing with best-laid plans:

Traders talk about their ‘uncle points’. When someone is twisting your arm out of its socket, there will come a point you’re in so much pain that you have no choice but to cry ‘Uncle!’ and close out the position, no matter how much it humiliates you, or ruins all your plans.

Maybe you don’t plan to cash out your investments any time soon. But if you lose your job, or your marriage, or your house burns down, or a loved one gets sick, you might have to sell with the worst possible timing.

Can we protect against this failure mode?

Yes, but not perfectly. Uncle points can be eliminated by buying insurance, maintaining emergency funds, and generally having a plan for various unthinkable scenarios. There will always be some level of uncertainty, but you can greatly reduce the chances of getting your arm twisted at an inopportune time.

3. Lack of Surplus Income

Lots of people are in for a tough time; unemployment is forecast to hit 20 per cent. You can’t keep buying stocks if you don’t have a reliable source of surplus income.

Can we protect against this failure mode?

This is not really a ‘failure’, so much as a limitation in who can take part. If you’re nearing retirement, I guess you could consider working a little longer? I haven’t had a proper job in a while, but I’ll probably start doing a little more (paid) work for this same reason.

4. This Time is Different

The buy-and-hold-forever strategy does rely on one ‘insight’: the observation that humans steamroll over absolutely anything that comes between us and our incredible thirst for wealth creation: be it the Spanish Flu, two World Wars, the Great Depression, 9/11, the implosion of the financial system, whatever.

I am going to go out on a limb and predict that COVID-19 will one day join this list.

Could this time really be different? It’s always possible!

Past performance doesn’t predict future returns, and the world is only ever getting weirder. If global stock markets don’t recover in our lifetimes, something has gone so terribly wrong that the balance of our retirement portfolios is probably not gonna be top of mind, but it’s still an interesting question.

If the current situation has taught us anything, is that it’s entirely rational to be paranoid about vanishingly unlikely tail risk events.

I tried to model these kind of edge cases in Beware of Geeks Bearing Formulas. The general takeaway is that the year in which you happen to start drawing down your portfolio has a huge impact on your fortunes (think of someone who blissfully celebrated their retirement in 2019, and is now burning capital with the worst possible timing), but the window of history during which you’re accumulating doesn’t matter nearly as much.

This is one of the reasons I’m no longer keen on the whole ‘early retirement’ thing. It works out great for many people, but it’s a bit riskier than it appears.

Can we protect against this failure mode?

Kind of? The safest possible strategy—financially, and for life satisfaction—is to find work you enjoy, and do it forever. If that’s not possible, well, going long on human innovation and wealth creation has never failed us before. Hopefully this time is no different.

The Irresistible Appeal of Being Clever

OK. I put a very sexy headline on a very boring strategy that everyone already knows about. Why bother? Because, incredibly, this boring strategy that everyone knows about is still low-hanging fruit!

Consider that plenty of very smart people are incapable of taking this very simple and obvious advice; that the best investors are literal cadavers who are incapable of trading their accounts; that the guy who is telling you all this is a gigantic hypocrite who struggles to take his own advice.

I’ve been corrupted by working adjacent to the finance industry: a little knowledge is a dangerous thing. If you don’t know anything, and are worried about missing out on all these clever strategies you’ve heard your smart friends talking about, I give you permission to stop worrying.

This is one of those bizarre opportunities where carefully stewarding your ignorance and being as lazy as possible is almost certainly the best approach. It’s as if God made broccoli taste like chocolate; or we could defeat the greatest threat to human life in a generation by… staying home and sitting on the couch.

So, that’s the opportunity in front of us. The next few years will separate the boys from the men, the girls from the women, and the non-binary from the non-binary.

I promise to revisit this post in March 2025, so we can see whether it stands the test of time. If it holds up, and I manage to stop being clever long enough to actually follow my own advice, I will immediately become insufferably smug and start branding myself as a brilliant investing guru.

If it doesn’t hold up, and you’re salty, well. You’ll have to come find me and my reaver gang in the badlands of Mexico, and say it to my (steampunk apocalypse masked) face.

a real ad that amazon keeps showing me

ADDENDUM: Please stop emailing me asking for personal investment advice (please continue emailing me for literally any other reason!) Even if I had the time to carefully evaluate your individual circumstances and risk preferences (I don’t), and the competence and skills required to help you out one-on-one (I don’t), I’d be getting myself in legal trouble. For NZers: I’m obviously biased, but my friend Sonnie Bailey is an independent financial adviser and former lawyer who offers consultations and formal plans, including a new service he’s trialling for $99. If you have other recommendations—trustworthy advisers in your country, tools for modeling risk, further reading along these lines—please share them in the comments! 😎

Notes:

Footnotes

-

If you have the means to do so, you could keep paying any service workers you usually hire, like cleaners or hairdressers, and buy vouchers and gift cards for local businesses to use when the quarantine lifts. More tentatively: lobby your government to a) support precarious workers who are suddenly strapped for cash, and b) refuse bailouts for large corporations that returned billions to shareholders and management in recent years while making no provisions for lean times (with the exception of e.g. airlines, which are basically utilities these days). I am way too dumb to know if the economics of this are sound—Scott Sumner has thoughts—but I’m going to toss it out there anyway. ↩

-

In optionality terms: the most important thing is always to stay the hell away from anything that might turn out to be a Bottomless Pit of Doom. ↩

-

This problem gets even worse among the kind of smart people who know a lot about cognitive biases, because they think they’ve compensated for them, and end up even more overconfident. ↩

-

This might be a good time to confess that I’m currently testing a momentum (trend-following) strategy with a small part of my portfolio, which, uh… flies in the face of all of the above. It’s performed almost comically badly through the COVID-19 crash, which ought to have been a delicious punishment for my hypocrisy and hubris, except that I just so happened to over-rule the crucial decision (i.e, I got lucky). I’m also tracking the counterfactual where I stuck with the experiment: if momentum really does turn out to be a persistent anomaly in otherwise efficient markets, then that would be fascinating—either way, I’ll try to write up a review some time later this year. ↩

30 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 2 replies Hide replies

Show 1 reply Hide reply