Futurama is one of the greatest cartoons of all time. If you haven’t seen this gem of early noughties TV, here’s the basic premise: Pizza delivery boy Fry accidentally falls into a cryogenic freezer at the turn of the new millennium, and wakes up 1000 years in the future.

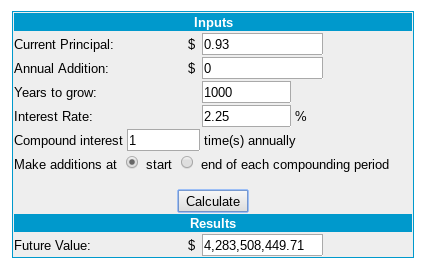

In the sixth episode, ‘A Fishful of Dollars’, Fry re-discovers his old bank account. At the time he was frozen, this contained the princely sum of 93 cents. After 1000 years spent as a human popsicle, he learns that the balance has compounded from less than a buck to the staggering sum of $4.3 billion. Hijinks and capers ensue.

While this is a neat idea for a plotline (and a lovely little homage to H.G Wells) casual viewers might assume the numbers involved were just made-up joke figures. But the cool thing about Futurama is that it was written by a bunch of boffins who take this sort of stuff seriously. How seriously? Well, Ken Keeler, who has a PhD in applied mathematics, invented a theorem purely to resolve a plot point in another episode. It ended up being published in an academic journal. There’s no way writers of this caliber would resort to using cartoon numbers.

And so, yes, 93 cents at 2.25 interest for 1000 years really DOES compound to to $4.3 billion. If you want to get pernickety, the exact figure is $4,283,508,449.71.

#theydidthemaths

Say it out loud: With enough time on your side, 93 cents can transform into $4.3 billion. If your gut instincts are screaming that this is staggeringly, ridiculously, wrong—well, you’re not alone.

Evolution has wired us up to think about the world in simple linear terms, because that’s how most of the things we see around us work. If you plant one seed, you get one carrot. If you produce one more dongle to sell, you earn one more dollar. Your hair steadily grows by a fraction of a millimetre each day; you don’t just wake up one morning looking like the lovechild of Tom Selleck and Wolfman.

While linear growth makes perfect intuitive sense, exponential growth is much harder to wrap our ape brains around. As Mark Zuckerberg put it: “Humans don’t understand exponential growth. If you fold a paper 50 times, it goes to the moon and back.”

This is a delicious example, not only because the imagery is so jarring—whoa, a tiny sheet of paper can do that?—but because the Zuck himself got it wrong. If you fold a piece of paper 50 times over, it doesn’t make a paltry return trip to the moon—it goes all the way to the freakin’ SUN. Humans don’t understand exponential growth, indeed.

Here’s one last example, from Abundance author Peter Diamandis:

“If I take 30 large linear steps (say one meter) from my Santa Monica living room, I end up 30 meters away, or roughly across the street. If, alternatively, I take 30 exponential steps from the same starting point, I end up a billion meters away, or orbiting the earth 26 times.”

me trying to come to grips with exponential growth

I like collecting these sort of wildly unintuitive examples, in the hopes that if I continue to melt my brain, it might start to grudgingly give exponential growth the sort of respect it deserves.

The reason this is important is that exponential growth is not just some cute piece of mathematical trivia. It’s a real-world phenomenon, and it has the power to either make you or break you. You’ll find exponential growth lurking behind debt, compound interest, and inflation, among many other things.

Those people who ‘get it’ stand to benefit enormously. As for those who don’t, they don’t just miss out—they also risk having it used against them.

The Ugly Side of Compound Interest: Debt

Religious leaders have long understood the ugly side of compound interest, which was called ‘usury’ in ye olden times. Pope Leo the Great condemned it as early as 440AD, it used to be illegal in several countries, and it’s still banned under Islamic law today.

Here’s an example of how things can get unholy: Let’s say you borrow $100 to get you through to next payday, for which the lender charges a monthly interest rate of 20 per cent. That’s only $20, so not exactly a big deal. However, when next month comes by, you’ve just had to get your car fixed, and you can’t quite get the money together. The lender slaps on another 20 per cent, and the hurdle gets slightly higher. Left unchecked, it wouldn’t take much more than a year before that extra $20 had spiraled into outstanding interest of almost $1000, and if you don’t pay up, well… you might just get the clamps.

He’s CHAMPIN’ for a clampin’!

These days, most countries have laws that effectively outlaw both usury and clamping. That means a debt rarely gets cartoonishly large before it all comes to a head, but it’s still not going to be pretty. Most ‘reputable’ lenders set their terms so you repay the original sum as slowly as possible, which means they can continuously milk you for interest payments over years or decades. Mortgages used to be a standard 15 or 20 years; now they’re 30 years, and no doubt some genius home loan company will soon start marketing even-more ‘affordable’ 40 year terms.

The simplest way to avoid the ugly side of compound interest is to never borrow money in the first place. Of course, that’s not always practical or even desirable. For those who do take on debt, repaying it as fast as possible is almost always a smart move.

The Ugly Side, Continued: Inflation

Being debt-free is an excellent start, but it’s not quite enough to break free from the exponential death spiral. Let’s say your grandad saved up $100, and put it safely under his mattress where the IRS couldn’t find it. Back in 1968, that was a decent chunk of cash. But because the supply of money floating around generally tends to inflate over time, it becomes just a tiny bit less valuable every year—typically around 2 per cent, on average.

In the short-term, grandad wouldn’t even notice the rot setting in. After a year, his stash would still have almost exactly the same purchasing power. But once again, the compounding effect creeps ever higher, constantly ratcheting up the magnitude of the destruction.

Wind the clock forward 50 years, and inflation has run at a cumulative total of 628 per cent. Grandad’s $100 note is still the same piece of paper, but it’s only worth a pittance compared to when he stashed it away—the equivalent of about $13. This is why old people always complain about how you used to be able to buy a Buick and a bale of chickens for seventeen cents.

Even at low levels, inflation is a force of nature that makes you a tiny bit poorer every day. Every dollar you save right now is going to roughly halve in value 30 years from now—and that’s assuming inflation behaves itself, which is no guarantee. Just ask Zimbabwe.

Being a trillionaire: nowhere near as cool as it sounds.

And so, unless there was a period of very strange monetary policy stretching 1000 years, almost all of Fry’s gains would have been wiped out by the ravages of inflation.

Assuming inflation averaged 2 per cent a year, he’d be left with the equivalent of $11.29 when he woke up, which is somewhat less exciting than $4.3 billion. And of course, seeing as he didn’t stash his cash under his mattress like grandpa, the taxman would have dipped his sticky fingers in too, meaning that original 93c would in fact have long since disappeared into the void.

The Beauty of Compound Interest

Good news, everyone! In spite of everything you’ve just heard, compound interest is still a truly wondrous and beautiful thing. You just need to get enough momentum going to break free from the opposing forces, and then you’re up and away.

To recap: Parking your money in the bank basically means you’re losing money very safely. To beat inflation, you’d have to move some of your savings into investments that pay a higher rate of return.

What would happen if Fry had stashed his money in the stock market? Going by the last couple hundred years of returns, he would have enjoyed a compound annual growth rate of almost 10 per cent. After accounting for inflation and tax, let’s be conservative and say the ‘real’ rate of return was closer to 6 per cent. Now, instead of ending up with $11.29, Fry has a fortune so fantastically large I can’t figure out how to say it in words, but I’m pretty sure it looks something like $18,800,000,000,000,000,000,000,000 (a sum so vast that in the act of rounding it down to a clean number, I’ve carelessly shaved off countless trillions).

Eagle-eyed critics will now proceed to ruin all the fun by pointing out that not everyone has a spare 1000 years on their hands to hang around in a cryogenic locker waiting to get rich. Nothing gets past you people! Fortunately, all is not lost: We can still reap the rewards of exponential growth in our own brief candle-flicker of a lifetime.

Let’s go back to grandpa and his mattress stash. If he invested that $100 instead, it’d make him $6 in the first year, which is pretty hard to get excited about. But the following year, the interest would start accruing on that $6, as well as the original deposit. After three years, he’d be earning interest on top of interest on top of interest, and so on.

By the end of the period, he’d be earning more than $100 a year in interest payments alone, and his original investment would have turned into $2000—and that’s adjusted for inflation. In today’s dollars, it’d be more like $5000.

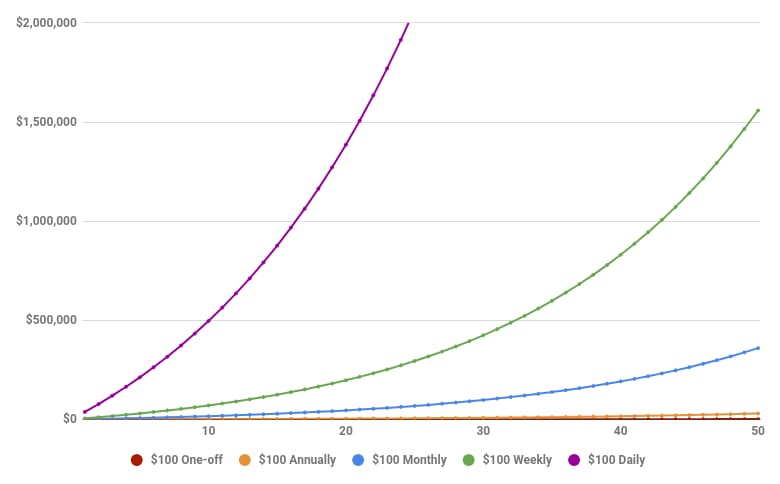

This is pretty exciting. But you can’t really expect to invest a chunk of money once, and then kick back and relax for the rest of your life. Investing steadily over time is the way to go, because it combines the compounding magic with the simple cumulative effect of making small contributions.

Instead of socking away $100 and then resting on our laurels, let’s sock away $100 a week—an easy target for most middle-class earners. This time, we end up with a cool $1.5 million. If we sock away $100 a day, which is doable for experienced frugalistas on the higher end of the income scale, we come away with $11 million. Sweet three-toed sloth of ice planet Hoth!

This savings rate is so astronomical that I had to chop most of it off the graph, but it’s a bit silly to extend it out that far anyway—most people would switch from hardcore saving mode to spending once they’d accumulated the first million or two, which as you can see on the chart, would only take 15 years or so. Definitely food for thought.

The Most Powerful Force in the Universe

Investment income is an easy and relatively safe way to reap the rewards of exponential growth, but there are other ways to get exposure: choosing a career or side-hustle with scalable, non-linear payoffs (see the barbell strategy), or making strategic investments in speculative businesses with the potential for exponential revenue growth (see the bastard’s barbell).

The principle of cumulative advantage operates on pretty much everything; from the arrangement of stars in the sky, to the height of trees, to income inequality, to the process of getting and staying in shape. Success tends to beget more success, while entropy, left unchecked, rapidly leads to the abyss. It’s actually pretty freaky how often this pattern crops up in seemingly unrelated domains (I might write more on this in another post).

For now, let me finish with an appeal to authority: if a silly cartoon doesn’t do anything for you, perhaps you’ve heard of a bloke called Albert ‘Big Juicy Brain’ Einstein. According to everyone’s favourite genius, compound interest is not only “the greatest invention in human history” (take that, polio vaccine!) not only “the eighth wonder of the world” (bite me, Machu Picchu!) but, in fact, “THE MOST POWERFUL FORCE IN THE UNIVERSE”. Now that’s what you call unequivocal.

…OK, fine, so Einstein probably didn’t actually say those things, but never a truer word has been spoken fabricated. Compound interest truly is a force of nature, and you don’t need to be an astrophysicist with an IQ of 160 to take advantage of it—hell, even a humble pizza-delivery boy could manage it.

THE END

7 Comments

Comments are archived from the original site. To respond, get in touch via the contact page.

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply

Show 1 reply Hide reply